This past summer, Heather Young attended the PACT conference in Nova Scotia, and ran into arts administrator Alan Wrenshall, who shared how much they enjoyed Heather's Finance for the Arts in Canada books! Alan was kind of enough to answer some questions we sent their way - enjoy!

Tell us a bit about yourself, and your arts administration role!

Alan Wrenshaw (left) and Heather Young at the 2025 PACT conference

My name is Alan Wrenshall (they/them) and I am a Queer, neurodivergent arts administrator for theatre, currently working as the Managing Director of Playwrights' Workshop Montréal. Founded in 1963, PWM is a nationally-mandated play development centre devoted to exploring and advancing artistic practices that support the creation of new works. To give you a sense of scale, in an average year, PWM collaborates with 250 artists and supports the development of more than 70 new works or translations.

Like many arts admin before me, I began my career in theatre as a Stage Manager, working behind the scenes on productions across Ontario. I gained invaluable experience and skills as an SM and loved being part of the creation process, but when Covid hit I briefly left the arts. Theatre kept calling me back though, and I moved to Montéal to join PWM’s administration team as a Coordinator. The previous MD left shortly after I started, and with the support of the rest of the team, I was able to take on the role. I'm incredibly grateful for the whirlwind opportunity that brought me here and the projects and artists we've been able to collaborate with.

Why did you purchase "Finance for the Arts in Canada," and how has the book met that initial need? Do you think it might be of use to others?

As a Stage Manager turned arts admin, my experience with budgets and finances before getting into arts admin was limited to say the least. Despite taking (most of) an accounting course in University, I did not have training in business. I knew the basics, but, in reality, the biggest budget I'd had to manage up to that point was for one production at a time. If Stage Managing taught me anything, though, it was how to be resourceful in finding information. The toughest part for me was sorting through all of the information that doesn't quite apply to arts nonprofits in Canada. Heather Young's Finance for the Arts in Canada was recommended to me by someone who had worked in my role previously to help me round out my knowledge and skills.

Which section or concept in the book did you find most valuable or impactful?

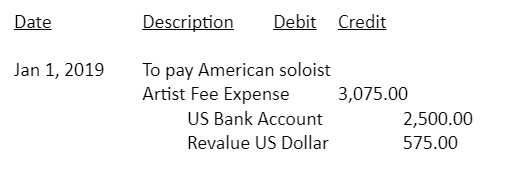

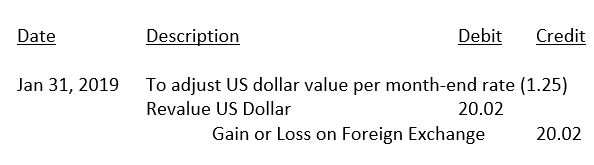

For me, the sections that Heather included on understanding more about Accounting principles and financial documents were the most helpful. Sections such as detailing what a trial balance is, or how the purpose of the balance sheet differs from that of the income statement, or what information you get from a statement of cash flow. Coming into the role I felt comfortable with budget tracking and planning, but having a resource that helped me understand the context for why the accounting processes are the way they are, and the different information they are collecting or intended to explain gave me a much more fulsome ability to engage with that part of my job.

Who would you recommend read this book, and find it useful?

I recommend this book to anyone who has taken on an arts leadership role and is stepping out of their comfort-zone working with running a business, or finances and accounting. I know that there are other new arts leaders out there that come from an artistic background with minimal finance experience, but want to learn. Concepts are explained clearly and thoughtfully. Even for topics you feel comfortable with, it's a great resource to be able to refer back to. It felt like being able to ask my bookkeeper questions without flooding her inbox, and gave me a better vocabulary for speaking with the auditor and my Board. I think it's useful information for anyone!

Many thanks to Alan for sharing their perspective with us!

You can learn more about Finance for the Arts in Canada here: youngassociates.ca/explore-book